The Portfolio That Doesn't Break

A brief history of hedging, and why most investors only learn it the hard way

Over the years as a wealth manager i gradually realized that most of my clients prove to be less tolerant of risk than their investor profile indicates. This naturally led me to focus on optimal hedging based on the client’s profile. Not so much their investor profile, but rather their emotional and psychological profile. Extreme hedging kills returns, but optimal hedging lets your clients (and yourself) sleep soundly.

If you’re a portfolio manager or wealth manager, failing to consider hedging could be your ticket to losing everything you’ve built up to events you can’t control or predict, such as bear markets or instant crashes.

A little history about hedging

There's a story about Thales of Miletus that most finance professors skip.

Around 580 BC, the Greek philosopher (better known for geometry and cosmology) made what is arguably the first recorded derivatives trade in history. Observing the stars and weather patterns, he predicted an exceptional olive harvest. Months before the season, he quietly paid small deposits to secure the rights to use every olive press in the region of Miletus and Chios. When the harvest came and demand for presses exploded, he rented them out at whatever price he chose.

Aristotle documented this in Politics as proof that philosophers could get rich if they wanted, they simply chose not to. But what Thales actually demonstrated was something far more enduring: you can profit from uncertainty, or you can protect yourself from it. The instrument is the same. The intention is what differs.

Fast forward 2,600 years. The instrument has evolved: options, swaps, inverse ETFs, volatility derivatives and more. But the underlying logic is identical. A hedge is not a bet against the market. It’s a decision to pay a premium today in exchange for reducing the damage tomorrow.

Most investors never make that decision. Until they have to.

The Illusion of the Safety Net

For most of the post-2008 era, investors didn’t need to think much about hedging. Central banks had effectively underwritten the market. Every dip was a buying opportunity. Volatility was something that happened to other people.

Then came 2022.

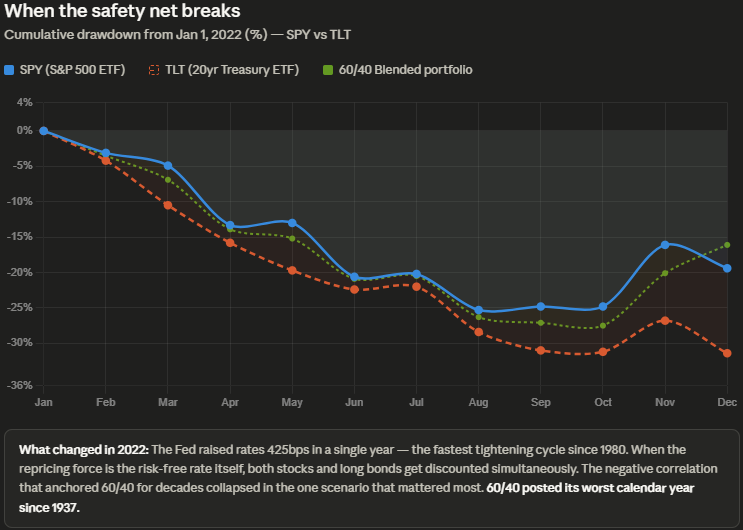

That year broke something that had been considered a near-law of portfolio construction: the negative correlation between stocks and bonds. The classic 60/40 portfolio (60% equities, 40% fixed income) was built on the assumption that when stocks fell, bonds would rise, cushioning the blow. Investors had trusted this relationship for decades.

In 2022, both fell simultaneously. Hard.

The S&P 500 dropped roughly 20% for the year. Long-duration Treasuries (TLT) fell over 31%. A traditional 60/40 portfolio posted its worst year since 1937. The hedge wasn’t a hedge anymore, it was just another losing position with a different ticker.

What happened? Inflation. When the driving force is a simultaneous repricing of the risk-free rate, everything gets discounted at a higher rate. Stocks and bonds become positively correlated precisely when you need the opposite. The diversification was real until the one scenario where it stopped being real arrived.

This is the central illusion of the safety net: diversification and hedging are not the same thing. Diversification spreads risk across assets that usually don’t move together. Hedging structures an explicit protection against a specific risk, regardless of what correlations do.

Understanding that distinction is the beginning of building a portfolio that doesn’t break.

What Hedging Actually Costs — And Why That’s the Point

Here’s the part nobody likes to talk about: hedging costs money. Always. If it didn’t, everyone would do it, and it would cease to function.

The cost takes different forms depending on the instrument:

Buying put options on an index means paying a premium that expires worthless most of the time

Holding gold or short-duration bonds means accepting lower expected returns during bull markets

Maintaining cash positions means sitting out compounding during rallies

Using VIX calls means paying for protection on volatility spikes that may never materialize (i never use this)

This is called the hedge drag: the performance cost of carrying protection. And it’s real. An investor who maintained a 5% allocation to long VIX exposure or protective puts throughout 2010–2019 would have underperformed a naked equity portfolio significantly every single year, until March 2020 arrived.

The question is never whether hedging costs something. It always does. The question is: what is the cost of not hedging, measured in the one scenario that actually matters?

Universa Investments (the tail-risk fund advised by Nassim Taleb) answered that question empirically in March 2020. While the S&P 500 collapsed 34% in 33 days, Universa’s tail-risk strategy returned approximately +3,600% for the month. The fund had spent years paying premiums on deep out-of-the-money puts. Most months those puts expired worthless. In March 2020, they didn’t.

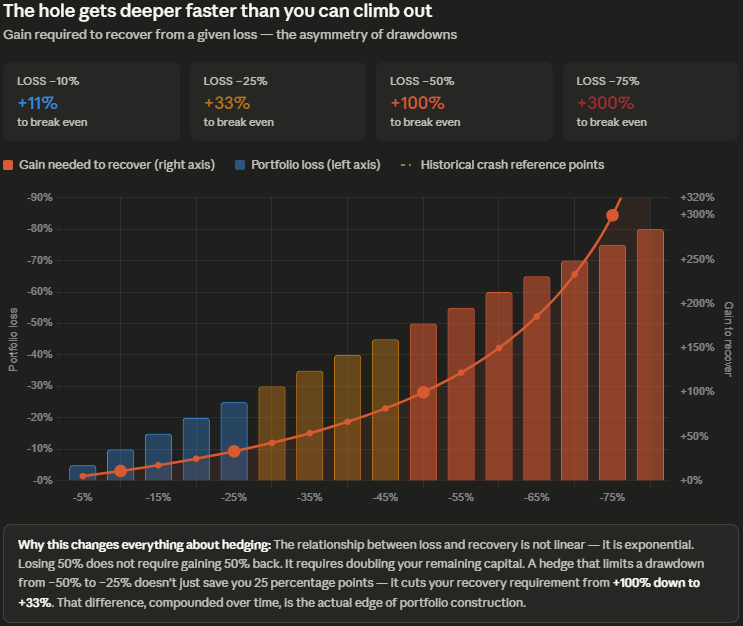

The math of recovery is asymmetric and unforgiving. A portfolio that falls 50% needs a 100% gain just to break even. A portfolio that falls 20% needs only 25%. Reducing the depth of the drawdown is not just psychologically valuable, it is mathematically decisive for long-term compounding.

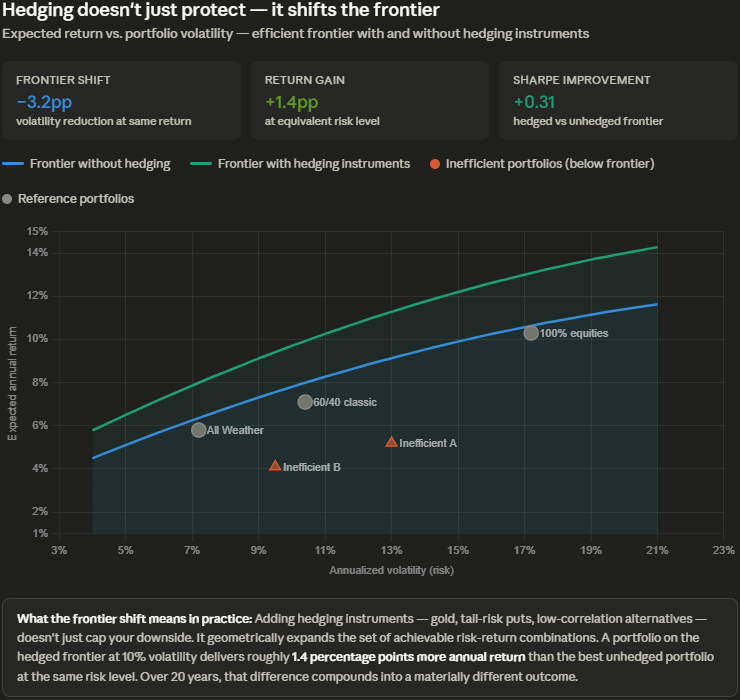

The Efficient Frontier: With and Without Hedges

Modern Portfolio Theory, as Markowitz formalized it in 1952, gives us the concept of the efficient frontier: the set of portfolios that maximize expected return for a given level of risk, or equivalently, minimize risk for a given expected return.

Every portfolio that falls below the frontier is suboptimal. You are accepting more risk than necessary for the return you’re getting, or accepting less return than possible for the risk you’re bearing.

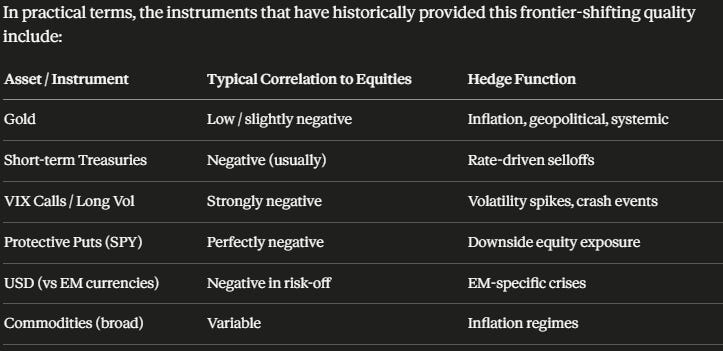

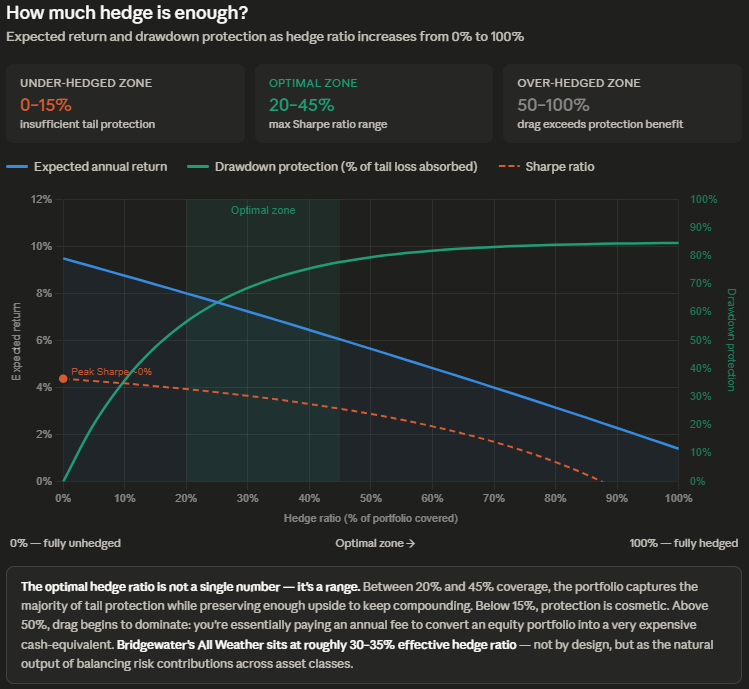

Adding hedging instruments: assets with low or negative correlation to the core portfolio, or explicit derivative structures, doesn’t eliminate risk. But it does something subtle and powerful: it shifts the frontier itself. A portfolio that includes effective hedging can reach the same expected return at lower volatility, or higher expected return at the same volatility.

The critical insight is that no single instrument hedges all risks simultaneously. Gold failed to protect in 2008's initial crash. Bonds failed in 2022. Cash gets destroyed by inflation. Effective hedging is a structure, not a single position.

Bridgewater’s All Weather Portfolio offers a clean real-world illustration of this logic. Rather than targeting a specific hedge ratio, Ray Dalio built a portfolio balanced across risk contributions rather than capital allocations. Equities, long bonds, gold, and commodities each contribute roughly equal amounts of volatility to the total portfolio, so no single regime wipes out the whole structure.

The result: in 2008, when a traditional 60/40 portfolio lost roughly 25–30%, All Weather fell approximately 3.9%. Not zero. But the drawdown was shallow enough that recovery was fast, and compounding was preserved.

What 2026 Actually Looks Like

The hedging calculus today is genuinely different from any prior decade. Four dynamics make it more complex and more necessary:

1. Correlation instability. The 2022 episode wasn’t an anomaly. As inflation regimes persist or return intermittently, the stock-bond correlation will remain unstable. You cannot assume negative correlation when building a defensive portfolio structure. Today, the liquidity generated by the Fed post-pandemic seems to be going 100% into equities. The retail sector currently has equity levels like never before in history.

2. Geopolitical fragmentation. The energy thesis documented in detail elsewhere: Hormuz, OPEC+ fractures, new global players and alliances, the Petro-LNG Dollar. All of them represents precisely the kind of regime uncertainty that traditional portfolio models don’t price. These are fat-tail events with non-trivial probabilities in the current environment.

3. Gold’s broken relationship with real rates. Historically, gold moved inversely with real interest rates. That relationship has decoupled meaningfully since 2022. Central bank accumulation (particularly from China, India, and Gulf states) has driven demand independent of rate dynamics. Gold is no longer purely a rate hedge. It is increasingly a systemic hedge against the dollar-denominated financial architecture itself.

4. Volatility is cheap until it isn’t. The VIX spent much of 2024 and early 2025 in historically suppressed territory. Cheap volatility means cheap insurance. The market’s complacency is, paradoxically, the best moment to buy protection, before everyone else remembers they need it.

The Premium Worth Paying

Thales paid a small fee for the right, not the obligation, to use those olive presses. The farmers who owned the presses thought they were the smart ones, collecting upfront cash while Thales speculated on weather patterns.

When the harvest came, the framing inverted.

The deepest lesson of hedging isn’t technical. It’s psychological. It requires paying a real cost, consistently, for protection against something that hasn’t happened yet and may feel increasingly unlikely to happen the longer the market cooperates.

The investors who do this well don’t think of it as insurance. They think of it as the price of staying in the game long enough for compounding to do its work.

Because a portfolio that survives intact through a crash doesn’t just avoid losses. It’s the one left with capital to deploy when everything is cheap.

That is the edge. Not the hedge that pays off but the discipline to carry one before you need it.

Hedging isn’t for everyone. For investors with strong convictions and high risk tolerance (like myself), hedging isn’t advisable. But for people unfamiliar with this world, not being hedged can mean panicking at times when you need to stay calm and avoid emotional decisions. And for a portfolio manager or wealth manager, it can mean retaining clients who, without that protection, would have panicked.

As always, the best approach is to have a thorough understanding of what we’re buying, not just looking at prices or charts, but knowing in detail what each company in our portfolio does, its risks, its competitors, its moat, and its management. With more information, we pay less attention to the constant noise of the markets.

This post is for educational purposes only. It is not financial advice and does not represent an investment recommendation. Always do your own research.

What's your thought on BLNDX as a All Weather portfolio?

Thank you for the well-written primer on risk-adjusted returns. One interesting consideration is your point about a hedge being specific to a particular risk. So what one is actually trying to hedge against is critical to portfolio construction.

If gold is a hedge against fiscal debasement, then owning it is about preserving purchasing power over a long time frame. Gold is unlikely to be a good hedge against short-term liquidity-driven volatility (where everything becomes correlated). While other hedges that offer little or negative correlation to equity/credit volatility are preserving short-term purchasing power by reducing exposure and draw downs.

So the challenge I personally have is in thinking about those two complementary objectives and how to balance my portfolio accordingly. The question becomes how much gold/royalties/etc. to hold versus other types of hedges? The implication seems to be that your optimal range also has within it an optimal balancing between types of hedges.

I’m happy to hear others thoughts. What do you think?